What is an FHA Streamline Refinance?

If you currently have an FHA loan and are looking to lower your monthly mortgage payments, an FHA Streamline Refinance might be the perfect solution for you. Also known simply as an FHA Streamline or FHA Streamline Refi, this mortgage program is designed to make refinancing as quick and painless as possible. By requiring less documentation and typically no home appraisal, homeowners in Dunedin, FL, can secure better interest rates with minimal hassle.

At Mortgage Info by Sean, we specialize in helping Florida residents navigate their home loan options. Whether you are seeking a standard rate and term refinance or exploring specialized government programs, we have the expertise to guide you. We are also experts at providing second opinions on FHA streamline refinance applications, ensuring you get the absolute best terms available.

The primary goal of an FHA Streamline Refi is to provide a net tangible benefit to the borrower. This usually means a lower interest rate, a reduced monthly payment, or transitioning from an adjustable-rate mortgage to a stable fixed-rate loan.

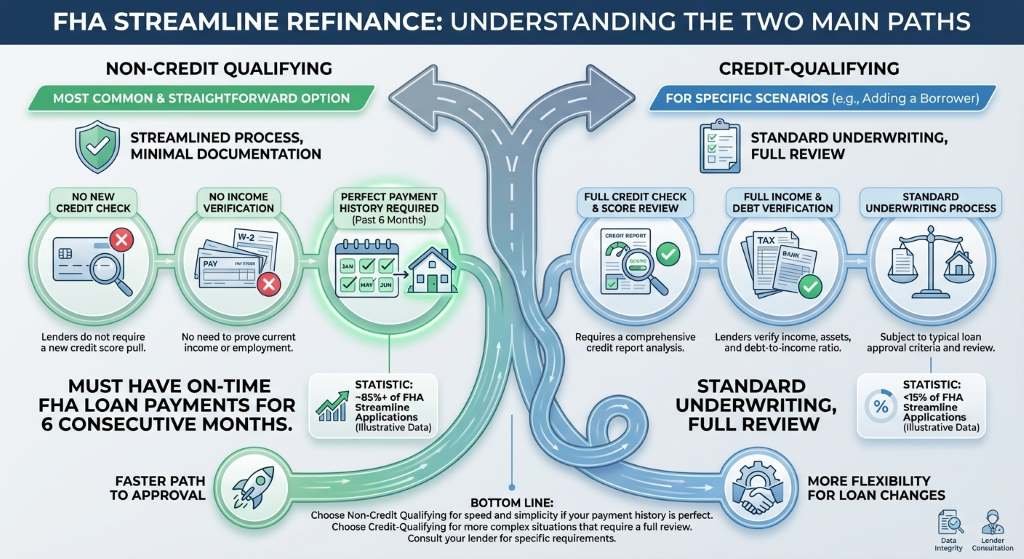

Credit-Qualifying vs. Non-Credit Qualifying FHA Streamlines

When you apply for an FHA Streamline Refinance, you will generally choose between two main paths: credit-qualifying and non-credit qualifying. Understanding the difference is crucial for a smooth loan process.

- Non-Credit Qualifying FHA Streamline: This is the most common and straightforward option. Lenders do not require a new credit check or income verification. As long as you have a perfect payment history on your current FHA loan for the past six months, you can generally qualify. It is incredibly efficient, much like the VA Interest Rate Reduction Refinance Loan (IRRRL) for eligible veterans.

- Credit-Qualifying FHA Streamline: This option requires the lender to verify your income and pull your credit score. You might choose this route if your financial situation has improved and you want to ensure you get the lowest possible interest rate, or if a borrower is being removed from the mortgage title.

If you are unsure which path is right for your unique situation in Dunedin, Sean McManamon is here to help. We evaluate your current mortgage, your financial goals, and your long-term plans to recommend the optimal refinancing strategy.

| Feature | Non-Credit Qualifying | Credit-Qualifying |

|---|---|---|

| Credit Check Required | No | Yes |

| Income Verification | No | Yes |

| Appraisal Needed | Typically No | Typically No |

| Best For | Fast processing and simply lowering your rate | Removing a borrower or proving improved credit |

| Payment History | Flawless for the last 6 months | Flawless for the last 6 months |

Why Get a Second Opinion on Your FHA Streamline Refinance?

Not all mortgage lenders offer the same rates, fees, or level of customer service. Even with a standardized program like the FHA Streamline Refinance, lender overlays (extra rules imposed by individual banks) can complicate your approval or increase your overall costs.

That is exactly why getting a second opinion is a smart financial move. We are experts at providing second opinions on FHA streamline refinance offers. When you bring your initial Loan Estimate to Sean McManamon, we will review it line by line. We often find hidden fees or higher-than-necessary interest rates that we can beat.

Benefits of working with a local Dunedin, FL mortgage consultant:

- Personalized Strategy: We schedule a strategy consultation call to understand your specific needs.

- Transparent Processing: From pre-approval to closing, we keep you informed every step of the way.

- Local Expertise: We know the Florida real estate and lending market inside and out.

Q1: Do I need an appraisal for an FHA Streamline Refinance?

In most cases, no. One of the biggest benefits of an FHA Streamline Refi is that it typically does not require a new home appraisal, meaning you can refinance even if your home’s value has decreased.

Q2: Can I get cash out with an FHA Streamline?

No, the FHA Streamline program is strictly for lowering your interest rate or changing your loan term. If you need cash out, you will need to apply for an FHA Cash-Out Refinance, which requires a full credit check and appraisal.

Q3: What are the basic requirements to qualify?

You must currently have an FHA loan, have made at least six consecutive on-time payments, and the refinance must result in a net tangible benefit, such as a significantly lower monthly payment.

Q4: Are there closing costs with an FHA Streamline Refinance?

Yes, there are closing costs. However, lenders can sometimes offer a no-cost refinance by charging a slightly higher interest rate to cover these fees, or you may be able to roll certain costs into the loan amount depending on the specific terms.

Q5: How fast can an FHA Streamline close?

Because there is less paperwork and usually no appraisal required, an FHA Streamline Refinance can often close much faster than a traditional refinance, typically within 30 to 45 days.

Contact Sean McManamon Today for Your FHA Streamline Second Opinion